From Concept Validation to Scalable Breakthrough

Decentralized Physical Infrastructure Network (DePIN) is an innovative network architecture that integrates blockchain technology with physical infrastructure. It leverages blockchain-based token incentive mechanisms to attract individuals and enterprises to contribute physical resources such as storage space, computing power, and network bandwidth, thereby establishing a distributed shared infrastructure network. Its application scenarios widely cover multiple fields including decentralized storage, wireless networks, and AI computing power support. Unlike the construction model of traditional centralized infrastructure, DePIN breaks the monopoly of major players over core physical resources with its low-cost and scalable advantages, forming a unique ‘co-construction and sharing’ industrial ecosystem.

The concept of DePIN gradually took shape as blockchain technology penetrated the real economy, with its early landmark beginning marked by Helium’s initiation and gradual rollout of a distributed wireless network project in 2013. This project incentivized users to deploy hotspot devices to build a low-power Internet of Things (IoT) network, providing the first implementable practical sample for the DePIN sector. In its early stages of development (2019-2020), DePIN remained in the phase of conceptual exploration and small-scale validation, with projects mainly focusing on technical feasibility testing. The number of devices within the ecosystem was limited, application scenarios were singular, and the sector did not gain widespread attention in the cryptocurrency industry.

The year 2021 became a turning point for the DePIN sector. As the Web3 industry’s demand for real-world implementation grew, along with the collaborative development of AI and IoT technologies, capital began to flow in at an accelerated pace. A group of projects focused on computing power, data collection and transmission, wireless communication, and sensor networks emerged one after another, leading to the initial expansion of the sector. By 2024-2025, the industry completed the crucial transition from concept validation to revenue-driven growth. Despite experiencing market capitalization fluctuations, high-quality projects achieved breakthroughs through sustainable revenue. Regulatory advancements further cleared obstacles for sector development, propelling DePIN from a niche technological concept towards large-scale industrial applications.

Since the emergence of the concept, the landscape and scale of the DePIN sector have exhibited significant volatility. In its early stages, due to immature technology, ambiguous business models, and insufficient demand-side momentum, the sector’s scale remained stagnant for a prolonged period. From 2023 to early 2024, driven by the热度 of the cryptocurrency market, the total market capitalization of the sector once again rose rapidly, with a surge in the number of projects. However, most projects relied on financing rather than actual revenue, showing clear signs of泡沫化. In 2025, the market underwent a deep回调, with market capitalization shrinking significantly. At the same time, projects lacking real application value were eliminated by the market, while those with genuine scenario demands stood out. The sector’s landscape gradually shifted from ‘unbridled growth’ to ‘high-quality and精细化 development,’ forming an industrial structure centered around leading projects and characterized by multi-domain协同 development.

(I) Industry Overview

1.1 The year 2025 marks the turning point for DePIN from concept validation to revenue realization.

During 2024-2025, the DePIN industry officially moved beyond the concept validation phase and entered a new era of revenue-driven规模化 development. Although the market experienced severe value adjustments, with total market capitalization falling from $30 billion at the beginning of 2025 to around $12 billion by the end of the year, this ‘survival of the fittest’ type of fluctuation instead promoted良性 iteration within the industry—high-quality projects with sustainable revenue capabilities not only survived but also achieved steady growth. During this period, the number of active projects in the sector increased from 295 to 433, and the number of network devices grew from 1.9 million to over 42 million. Leading DePIN projects generated annual revenues exceeding $57 million, demonstrating the feasibility of commercial落地 in the sector.

In terms of project deployment across public blockchains, Ethereum leads in the number of projects, followed closely by Solana, showcasing strong ecosystem appeal. Polygon and peaq rank third and fourth, respectively. Notably, peaq, as an emerging force in the sector, has seen continuous expansion of its ecosystem over the past year, growing into a significant participant that cannot be ignored. Meanwhile, DePIN projects within the Solana ecosystem have consistently maintained a leading position in the sector, demonstrating core competitiveness far surpassing industry averages in both network coverage breadth and revenue performance.

On the capital front, investment热度 in the DePIN sector remained strong in 2025, with over 40 financing rounds completed throughout the year. Projects such as Wingbits, Beamable, Geodnet, DoubleZero, Sparkchain, GAIA, Hivemapper, 375ai, Daylight, Nubila, Metya, DePINSIM, Space Computer, Gonka, Grass, Fuse Network, and DAWN all secured funding exceeding $5 million. Meanwhile, prominent institutions like Multicoin Capital, Framework Ventures, a16z Crypto, Borderless Capital, EV3, and Japan Display continued to actively participate in the sector, reflecting capital markets’ recognition of DePIN’s value and injecting ample momentum for technological iteration and规模化 expansion within the industry.

1.2 Inflection Point of Protocol Revenue

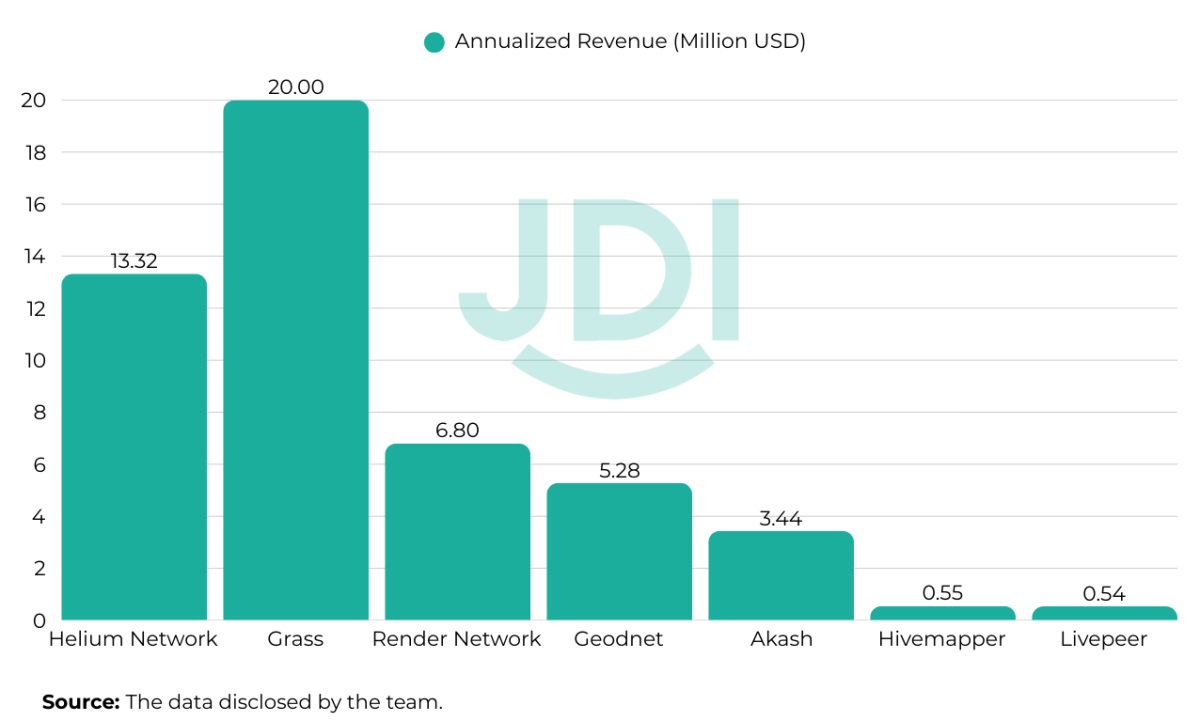

In 2025, the DePIN sector will reach a critical revenue inflection point, with leading protocols demonstrating clear and sustainable growth momentum. This will drive the sector’s annualized revenue to surpass $57 million, completely shedding the previous reliance on financing for a ‘blood transfusion’ development model. Specifically, top projects have shown remarkable performance: Helium Network’s revenue in Q4 2024 reached $3.33 million, representing a year-over-year increase of 255%, with an annualized revenue of $13.32 million; Grass has exhibited explosive growth potential, generating $2.75 million in revenue in Q2 2025, further increasing to $4.3 million in Q3, with projections showing Q4 revenue could surge to $12.8 million; Render Network achieved $1.7 million in revenue in Q3, growing by 144% quarter-over-quarter, with an annualized revenue of $6.8 million.

Additionally, Geodnet reported $1.23 million in revenue in Q3, reflecting a year-over-year growth of 216%, with an annualized revenue of $5.28 million; Akash maintained steady growth, achieving $860,000 in revenue in Q3, a 4% increase from the previous quarter, with an annualized revenue of $3.44 million; Hivemapper and Livepeer also showed strong performance in Q4, reaching $138,000 and $134,000 respectively, corresponding to annualized revenues of $552,000 and $536,000, with Livepeer recording a year-over-year increase of 83.6%.

Behind the revenue growth, a matrix of diverse drivers is emerging. On one hand, the rigid demand for computing power and data within the AI industry has become a core engine, directly driving rapid revenue growth for protocols focused on computational support such as Grass and Render Network. On the other hand, Helium Mobile’s mobile services experienced explosive user growth, surpassing 2 million registered users, contributing significantly to the sector’s revenue growth. Notably, the energy and mapping sectors are accelerating their rise, with related DePIN projects advancing their technical implementation, poised to become the third major revenue growth driver following ‘AI infrastructure’ and ‘mobile services’.

1.3 Regulatory Breakthroughs

In 2025, DePIN projects achieved breakthrough progress in U.S. regulatory areas, laying an important foundation for the industry’s compliant development. On April 10, the U.S. Securities and Exchange Commission (SEC) dismissed the lawsuit against Helium Network, explicitly ruling that its issued tokens—HNT, MOBILE, and IOT—as well as connected hotspot devices, do not constitute securities. This ruling not only cleared obstacles for Helium Network’s development but also effectively curtailed subsequent similar lawsuits against DePIN projects, providing key regulatory guidance for the entire industry.

On July 7, the Helium team held a special meeting with the SEC’s cryptocurrency task force, promoting clarification from regulators that digital asset issuance, trading, and consumer product sales within the DePIN ecosystem are not subject to federal securities laws. A jointly signed written opinion submitted by multiple DePIN organizations helped consolidate industry consensus and refine regulatory rules.

Further positive developments continued, with the SEC issuing no-action letters to DoubleZero’s $OO token on September 29 and Fuse Energy’s $ENERGY token on November 24, confirming that under specific issuance conditions, these tokens do not fall within the scope of securities.

These regulatory advancements mark a critical shift for the DePIN sector from ‘regulatory ambiguity’ to ‘clear compliance.’ By reinforcing a utility-driven development model, DePIN has shed the speculative label common in the cryptocurrency space, fostering constructive interactions with regulators. This not only reduces enforcement risks for the industry but also accelerates the entry of institutional capital, solidifying the regulatory foundation for scalable growth.

1.4 DePIN Hardware

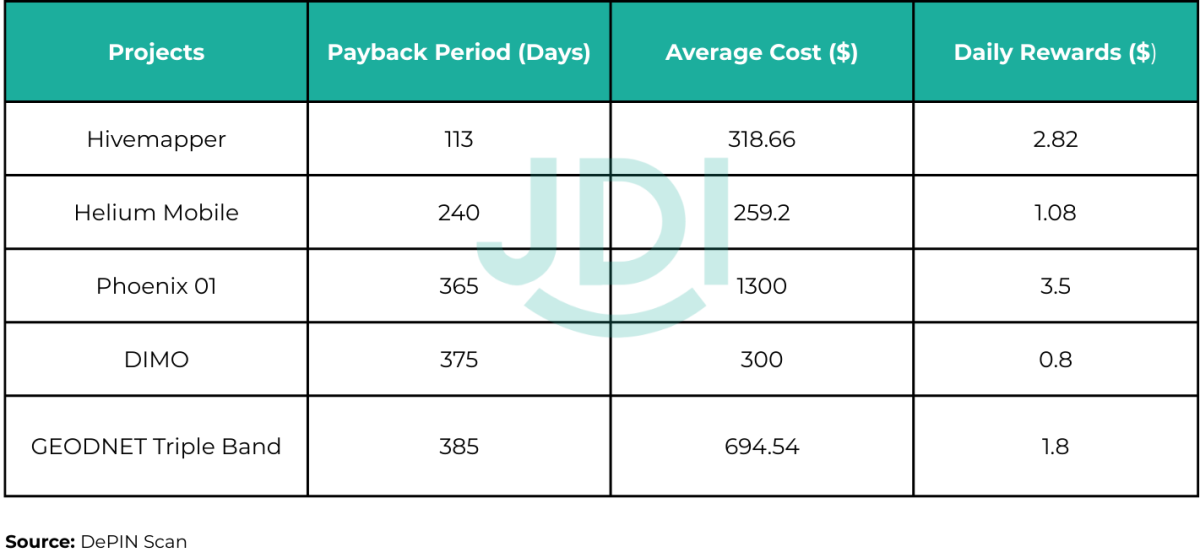

According to statistics from DePINScan, the total number of DePIN devices across the network has now exceeded 42 million. Hardware, as the core infrastructure supporting the operation of this sector, directly affects the stability and expansion efficiency of the DePIN network through its deployment and performance. Focusing on the sub-sector of DePIN hardware mining, a comparative analysis of three key indicators—hardware cost, daily earnings, and payback period—clearly reveals the differentiated competitive advantages of different categories of projects.

From the perspective of the payback period, sensor and wireless hardware mining projects stand out due to their moderate equipment costs and quick returns, making them the dominant category in this dimension. In contrast, server-based mining projects exhibit notable differentiation, with generally longer payback periods but lower technical barriers and flexible deployment options.

In terms of the shortest payback period, representative projects include:

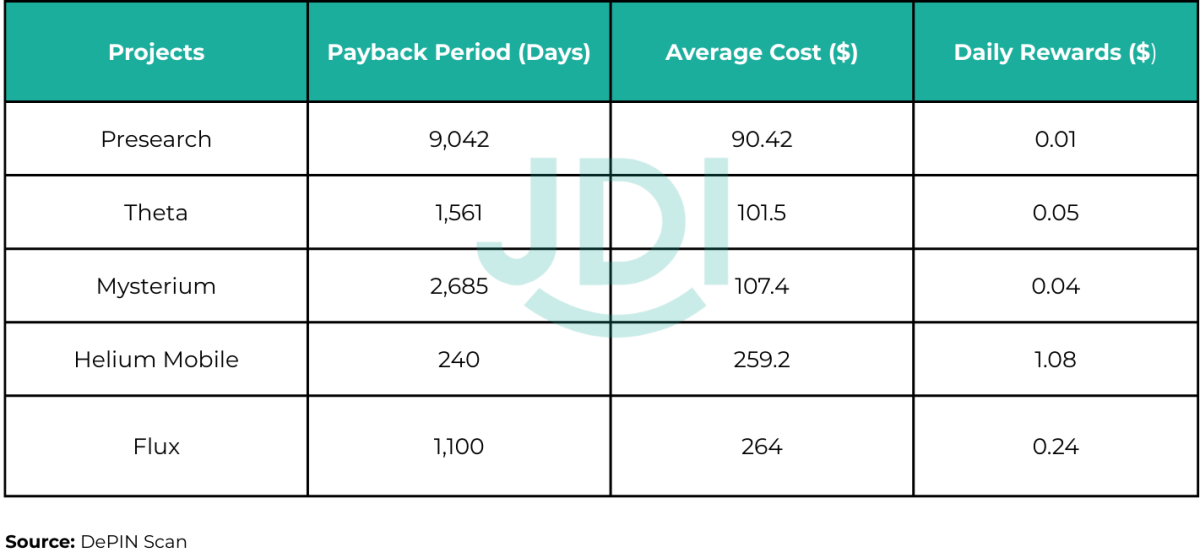

Regarding the lowest average mining costs (with priority given to ease of use), leading mining projects include:

1.5 Industry Risk Management Notice

In terms of risk management, DePIN projects must remain vigilant against uncertainties caused by changes in founders or business model adjustments. For instance, after Andy Chatham, the founder of DIMO, resigned in April 2024, DIMO transitioned to a subscription-based model where users are required to pay for vehicle data services. While this enhanced revenue stability, it also increased the risk of user attrition, necessitating attention to subsequent product iterations.

io.net also faced controversies due to team changes and a lack of transparency in fundamental data disclosures. For example, the community experienced a trust crisis regarding potential past issues involving CEO Ahmad Shadid; GPU quantity records were centralized, raising doubts about exaggeration, insufficient actual usability, and utilization rates. Despite rapid narrative and visibility growth, the project disclosed limited information about real computing power demand, stable customers, and ongoing protocol revenue. Its heavy reliance on token incentives raised concerns about network sustainability once subsidies were reduced.

Furthermore, compliance risks in the DePIN space cannot be overlooked. Taking Hivemapper as an example, the project collects mapping data via vehicle-mounted cameras, which sparked illegal surveying disputes in China. In October 2024, China’s Ministry of State Security reported on a foreign company’s illegal surveying activities, leading to the detention of some users operating Hivemapper devices, involving issues of cross-border data transmission and national security. This serves as a reminder that DePIN projects must strictly adhere to regional regulations, especially in data-sensitive fields, to avoid operational disruptions caused by compliance blind spots.

(II) Key Project Layout of Japan Display

Based on our assessment of the current stage of the DePIN sector, we believe it has begun transitioning into a phase of scaled breakthroughs driven by demand and actual revenue. The criteria for evaluating DePIN protocols are no longer metrics like “how many hotspots” or “how many nodes,” but rather “what percentage of traditional infrastructure has been replaced.” Over the past two years, we have systematically participated in and advanced nine main tracks with the clearest alternative paths around this central proposition.

2.1 Mobile Network: Helium Mobile

Helium Mobile is currently the only DePIN project that has outperformed traditional operators in real-world payment scenarios. Data from Q3 2025 shows that it has 540,000 paying users, with a peak daily active user count of 1.2 million, and a total of 115,000 hotspots (including 33,700 5G hotspots). The average monthly data consumption per user already exceeds that of similar traditional operator plans.

More importantly, the offload ratio: In 20 core cities across the United States, the Helium network has taken over 60% of community traffic, with some areas exceeding 75%. This means that, for the first time, the incremental market for mobile networks has seen a real-world case of community networks capturing a significant share.

The moat that traditional operators have relied on for the past three decades—’must build their own base stations, must incur massive capital expenditures’—is being dismantled by a model where ‘anyone can deploy hotspots, anyone can earn money.’

In 2025, Helium Mobile’s replication outside the United States is accelerating, with pilot cities in Southeast Asia, Latin America, and Africa showing hotspot densities in individual cities surpassing those of the local third-largest operators. The substitution logic in this sector has shifted from ‘feasible’ to ‘already happening.’

At the same time, Helium is building a value loop at the token level. Starting in October, Helium initiated a routine buyback program, repurchasing HNT tokens worth approximately $30,000 daily from the market. Over the past five months, nearly 1.5% of the total supply of HNT has been burned, with the current monthly burn rate stabilizing at 0.75%. Additionally, the Helium team disclosed that they are advancing explorations into HNT DAT services, planning to acquire HNT through both public and over-the-counter markets, and leveraging network-related revenue activities to further enhance the value support for each HNT token.

2.2 Centimeter-Level Positioning: GEODNET

GEODNET is now the world’s largest decentralized RTK network, with 21,000 active stations in 2025, covering 145 countries. Its Q3 revenue reached $1.2 million (a 27.9% increase quarter-over-quarter), and 6 million tokens were burned.

Traditional RTK annual fees range from $2,000 to $8,000, whereas GEODNET has reduced the annual cost for equivalent precision services to less than $100. It has been included in the official selection lists of leading agricultural machinery and surveying equipment manufacturers such as John Deere, DJI, and Topcon.

In major agricultural countries such as India, Brazil, and Indonesia, GEODNET is becoming the default option for centimeter-level positioning in new agricultural machinery. In Europe and North America, autonomous driving test fleets have begun adopting it as a low-cost redundancy solution.

Centimeter-level positioning is transitioning from ‘professional equipment’ to ‘public infrastructure.’ The long-term outcome of this shift is that an increasing proportion of the billions of dollars added annually to the global RTK market will flow directly into community networks rather than traditional suppliers.

2.3 AI Data Collection: Grass

Grass builds a verifiable, timestamp-complete public webpage dataset through users’ idle bandwidth. By 2025, its MAU will reach 8.5 million, covering 190 countries, with a daily data capture capacity exceeding 100TB.

Currently, the data provided by Grass accounts for 18%-22% of the incremental growth in major global open-source datasets, and some top AI laboratories have listed it as a regular supplementary source for daily training.

More importantly, it redistributes the authority to scrape public webpages from companies like Google, Meta, and Amazon back to end-users worldwide.

In the fourth quarter of 2025, Grass officially launched its iOS native client and real-time search interface, with APY stabilizing at 45%-55%, becoming the most direct way for ordinary people to participate in AI infrastructure.

The redistribution of data collection rights has already begun.

2.4 Distributed Energy Resource Network: Fuse Energy

Fuse Energy is a London-based energy technology company dedicated to building a decentralized renewable energy network. The company adopts the DePIN model, integrating various distributed energy resources, including solar photovoltaic panels, battery storage systems, electric vehicle charging stations, and smart meters, to provide users with energy equipment installation, power trading, and retail services. Currently, Fuse Energy operates 18MW of renewable energy assets and has over 300MW of projects under development. The company serves more than 150,000 paying customers, generates annual revenue of $300 million, and holds an energy supplier license, enabling it to directly provide demand response services to the UK grid.

To incentivize user participation in grid optimization, Fuse Energy introduced the $ENERGY token reward mechanism, encouraging users to adjust their electricity consumption during periods of abundant green power. This model converts actual grid dispatch requirements into verifiable, incentivized tasks on-chain, effectively combining energy behavior with token rewards.

Fuse Energy has not only demonstrated the feasibility of distributed energy networks in terms of large-scale operations and commercial implementation but also represents a forward-looking paradigm for energy collaboration. With actual operating assets, a continuously growing user base, and robust financial performance, the company has validated the significant potential of decentralized energy systems to enhance grid resilience, promote renewable energy integration, and incentivize user participation. Its practices have also revealed an important direction for DePIN: beyond building infrastructure from scratch, DePIN can achieve efficient coordination of existing facilities through ‘soft approaches.’ DePIN is not just about advanced technology; it is a system engineering project concerning incentives and collaboration. Fuse Energy’s success offers a replicable technological and commercial pathway for global energy transition.

In the energy sector, Starpower’s development is noteworthy but also highlights some latent risks in the industry. Starpower focuses on building virtual power plants (VPPs), enabling intelligent dispatch of distributed energy by connecting devices such as smart plugs, EV chargers, and batteries. In 2025, the mainnet of the project officially launched, expanding to thousands of sites and raising $4.5 million in funding, including $2.5 million led by Framework Ventures. However, Starpower’s model has sparked controversy: it serves as a reminder that DePIN cannot succeed simply by ‘plugging things in’—the real value lies in transforming these devices into tradable energy assets and ensuring dispatch efficiency and carbon credit transparency via blockchain. In reality, after shifting to a subscription model, the platform experienced increased user churn, partly due to device compatibility issues and maintenance costs exceeding expectations, resulting in actual dispatch efficiency falling short of promotional claims.

2.5 Green Energy Data Protocol: Arkreen

As one of the leading green energy data protocols, Arkreen is undergoing a qualitative transformation from ‘connecting data’ to ‘creating assets.’ Over the past year, Arkreen achieved several breakthroughs: over 300,000 global energy data nodes connected, 140 GWh of green energy tokenized, forming millions of dollars in on-chain green asset circulation, and burning 45 million AKRE tokens through protocol service fees, establishing a complete closed-loop from data connection to asset monetization.

In the future, Arkreen will advance three major pilot programs scheduled to launch intensively in the first quarter of 2026: a 300KW photovoltaic RWA project in Southeast Asia, bridging Web3 capital with physical green assets; the eCandle community shared power station project in Africa, addressing off-grid power supply challenges through on-chain payments; and an Australian ‘residential photovoltaics + Bitcoin mining’ pilot, converting surplus electricity into on-chain hard currency.

Three key milestones in 2025 lay the foundation for Arkreen’s long-term development: securing strategic investment from Robo.ai, a Nasdaq-listed company in Dubai, to accelerate exploration of the intelligent open machine economy; appointing Dr. Lin Jieli, former chairman of Hong Kong Cyberport, as a strategic advisor to support globalization and ESG mainstreaming; and promoting Merlin, a core community builder, to co-founder status, reflecting community-centric values.

In terms of token value, in addition to ongoing deflationary token burns, Arkreen is preparing large-scale incentive campaigns to explore mechanisms like RWA revenue dividends and DeFi integration, guiding token value recovery. Compared with projects like Daylight and Fuse Energy, Arkreen adopts a global, permissionless approach, constructing a Web3 energy network through off-grid system setups and surplus power computing solutions that decouple from traditional grids.

For the energy DePIN sector, Arkreen believes the convergence of computing power and electricity is a core trend that can address global energy imbalance issues. In 2026, Arkreen will focus on its existing strategy, completing the three pilots and achieving scalable replication, aiming to directly monetize energy assets by ‘trading electricity, generating Bitcoin, and serving AI models,’ advancing the evolution from green certificates to tangible power asset monetization. However, Arkreen’s globalization efforts have not been smooth sailing; for example, delays caused by data privacy regulations in some African regions resulted in limited project conversion rates, highlighting the regulatory uncertainties in emerging markets and their potential constraints on DePIN. We look forward to pioneers like Arkreen paving a more refined and seamless path for DePIN’s global compliance strategies.

2.6 Real-time Communication Protocol Layer: Datagram

Datagram provides a decentralized real-time communication infrastructure capable of supporting high-bandwidth, low-latency scenarios such as audio and video calls, gaming matches, and AI inference streams.

By 2025, the number of nodes will exceed 150,000, covering 120 countries, with an average available bandwidth per node of 80-120 Mbps. Over 200 enterprises have completed commercial deployment, with costs 60%-80% lower than traditional solutions such as AWS IVS, Agora, and Twilio. The core alternative logic is transforming real-time communication from ‘centralized cloud services’ into a ‘public protocol for global idle networks.’

Currently, Datagram accounts for 68% of real-time communication traffic in Web3 native applications and has begun to penetrate traditional gaming and video conferencing scenarios.

When latency-sensitive applications no longer need to pay a premium to cloud providers for bandwidth, the pricing power of communication infrastructure undergoes a fundamental shift.

2.7 Regional DePIN Operating System: U2U Network

U2U has achieved something more foundational in Southeast Asia: modularizing DePIN subnets. Any team can now deploy a dedicated wireless, computing, or storage network within days, compared to six months to a year previously.

By 2025, user growth will reach 150%, with TVL exceeding 150 million US dollars, supporting over 40 dedicated resource networks and becoming the de facto underlying infrastructure for new DePIN projects in Vietnam, Indonesia, and the Philippines.

Its emergence lowers the barrier to ‘building a DePIN project’ from requiring a core development team to only needing business logic. This is akin to extending the functionality of Cosmos SDK by one layer, transitioning from the era of public blockchains to the DePIN era.

In terms of traditional financial cooperation, U2U has established a deep partnership with SSID (SSI Digital Ventures, the technology arm of Vietnam’s largest financial institution, SSI Securities). SSID led U2U’s Series A round of 13.8 million US dollars, and both parties are jointly developing Vietnam’s first cryptocurrency exchange, expected to launch in Q1 2026. The exchange will integrate U2U subnets, support DePIN asset trading, and collaborate with partners like Tether and AWS to bridge traditional finance and the DePIN ecosystem.

Southeast Asia is becoming one of the regions with the highest density of global DePIN projects, with U2U being a direct driver of this phenomenon.

2.8 Aviation Data: Wingbits

Wingbits has achieved the disruption of a traditionally monopolized industry with minimal hardware costs: real-time global flight tracking.

By 2025, the network will exceed 5,000 sites, processing 13.1 billion data points daily, covering over 90 countries, and having signed data cooperation agreements with multiple airlines and regulatory bodies.

The core barriers of traditional players like FlightAware and Flightradar24—hardware deployment rights and data credibility—have been completely dismantled by community networks.

In Q4 2025, Wingbits officially validated its system via SpaceX’s Starlink, completely eliminating the risk of data spoofing. The redistribution of market share in flight tracking has shifted from ‘theoretical possibility’ to ‘currently happening’.

2.9 Spatial Mapping: ROVR

ROVR builds a decentralized high-precision mapping network using vehicle-mounted LiDAR sensors for autonomous driving and spatial AI. By 2025, the network will surpass 5,000 sites, covering North America and Europe, with $2.6 million raised in funding (led by Borderless Capital, with participation from GEODNET, etc.). Q3 revenue reached $800,000, marking a 45% increase quarter-over-quarter. Through AI-driven 3D data collection, ROVR provides real-time map updates to autonomous driving companies, reducing traditional mapping costs by 30%.

ROVR’s development demonstrates that DePIN can transform vehicles from transportation tools into data collection nodes, but it also faces challenges related to data privacy and LiDAR hardware compatibility. ROVR’s dataset includes petabytes of 3D point cloud data used to train autonomous driving models and AR/VR applications, accumulating over 10 petabytes of high-precision point cloud datasets. Community contributions enable real-time updates of urban roads and environmental changes, supporting map optimization for companies like Tesla and Waymo.

(III) Our Outlook on DePIN

In the next 3–5 years, DePIN is expected to evolve from ‘large-scale implementation’ to ‘multi-domain value release.’ We believe its synergistic development with embodied intelligence, AI data collection, energy and electricity, and AI hardware presents a significant opportunity to advance digital collaboration in the physical world.

3.1 DePIN and Embodied Intelligence

The development of embodied intelligence remains constrained by insufficient real-world interaction data and high deployment costs. The incentive and settlement mechanisms of DePIN have the potential to drive robots to engage in practical tasks at lower costs, generating environmental and operational data during execution that can feed back into model iteration. As robots gradually enter scenarios such as logistics, inspection, and home environments, a closed-loop of ‘task—incentive—iteration’ may emerge, enabling autonomous hardware to possess sustainable operational capabilities. Various networks are already exploring crowdsourcing robot data and distributed collaboration in this direction, while some projects provide opportunities to invest in early-stage robotics companies through asset tokenization models, such as BitRobot, OpenMind, Auki, Robostack, and XMAQUINA. If technology and regulatory environments permit, embodied intelligence could achieve faster real-world application.

3.2 The Potential of DePIN in AI Data Collection

High-quality, real-world data remains scarce. DePIN provides public incentive mechanisms for devices such as cameras, vehicles, edge terminals, and wearable devices, enabling continuous collection of real-time data like maps, videos, and multimodal inputs, addressing issues like lagging traditional training data and insufficient coverage.

In terms of data governance, blockchain has the ability to provide trusted traceability and privacy protection, potentially enhancing transparency in data quality and allowing individuals and device contributors to participate fairly in value distribution. The aggregation of multidimensional, real-time physical data at scale will become an important foundation for advancing AI model capabilities. Projects such as Sapien, Vader, and Rayvo are experimenting in this area.

3.3 Opportunities for DePIN in the Energy and Power Sector

The growth of distributed energy systems enables residential photovoltaics, energy storage, and charging equipment to potentially serve as network nodes. The DePIN mechanism can be used to promote collaborative scheduling of distributed resources and peer-to-peer green electricity trading, giving users more flexible options across power generation, storage, and consumption. Additionally, with rapidly increasing computational power consumption, if energy-side networks and AI-side demands can collaborate on-chain, this will have the potential to increase the utilization of green energy in digital infrastructure. We see projects such as Fuse Network, Arkreen, Daylight, Glow, and Sourceful Energy actively building in this space.

3.4 Reverse Advancement of AI Hardware on DePIN

As the costs of GPUs, NPUs, and communication modules decrease, the threshold for participating in DePIN is expected to continue lowering, allowing users to contribute computing power, storage, and networking capabilities via consumer-grade hardware. The widespread adoption of lightweight AI chips will promote node intelligence, enabling devices to possess self-adaptation and self-diagnosis capabilities, thereby reducing manual maintenance costs. Meanwhile, AI scheduling algorithms can dynamically allocate tasks, improving the utilization of idle resources and gradually evolving ‘point-like nodes’ into a sustainably operational network foundation.

Moreover, the thriving development of AI-powered smart hardware adds diversity to DePIN hardware, making it both profitable and compatible with richer functionality and playability.

We look forward to advancements in technology, incentive mechanisms, and governance models progressing together. The integration of DePIN with AI, energy, and hardware has the potential to reshape the way physical infrastructure collaborates, enabling real-world devices to gradually acquire ‘self-organization’ capabilities and creating new value-generating opportunities for industries.

As a core participant in the DePIN sector and a long-term contributor and industry leader in the DePIN hardware field, Japan Display will continue to focus on hardware innovation. It is committed to diversifying the product forms of DePIN hardware and expanding its functional boundaries. In the future, we will not only build a more diversified and scalable hardware ecosystem for the industry but also continue to support the growth of the DePIN sector. We will promptly share our cutting-edge insights and key perspectives with industry partners to jointly promote high-quality development in the sector.

Disclaimer and Risk Warning

The information in this article is for general reference only and does not constitute any financial or investment advice. The content (including project analysis and market data) is based on information available at the time of publication and may have timeliness issues.

Cryptocurrencies and related markets are highly volatile and risky, and past performance is not indicative of future returns. Readers must conduct their own due diligence, consult licensed advisors, and assess their own risk tolerance before making any investment decisions.

The author and publisher assume no liability for any losses or damages arising from the use of the information in this article or actions taken based on it. This article also does not constitute an offer to buy or sell any assets.