during Bitcoin A new ATH climbed above $ 111,000 in late May, a silent but measurable re -measured: More BTC is now kept more on external stock exchanges than organized platforms in the United States, and folder sizes are steadily leaking from places compatible with KYC.

The data from Cryptoquant shows that the market adopts institutional flows in 2025 without giving up its historical preference for its flexible cuddling and low -statistical trading platforms.

In this re -customization center is the exchange reserve rate, a procedure that compares the amount of BTC preserved to different types of stock exchanges. As of June 11, the precaution between KYC and ONGLECTS for exchanges decreased to 1.33, a decrease from 1.46 at the end of December.

The clouds of 9.1 % reflect a wider liquidity trend that quietly migrates from the places subject to regulatory, despite the start of the investment funds circulating in the immediate bitcoin in January and the subsequent flows it gave birth.

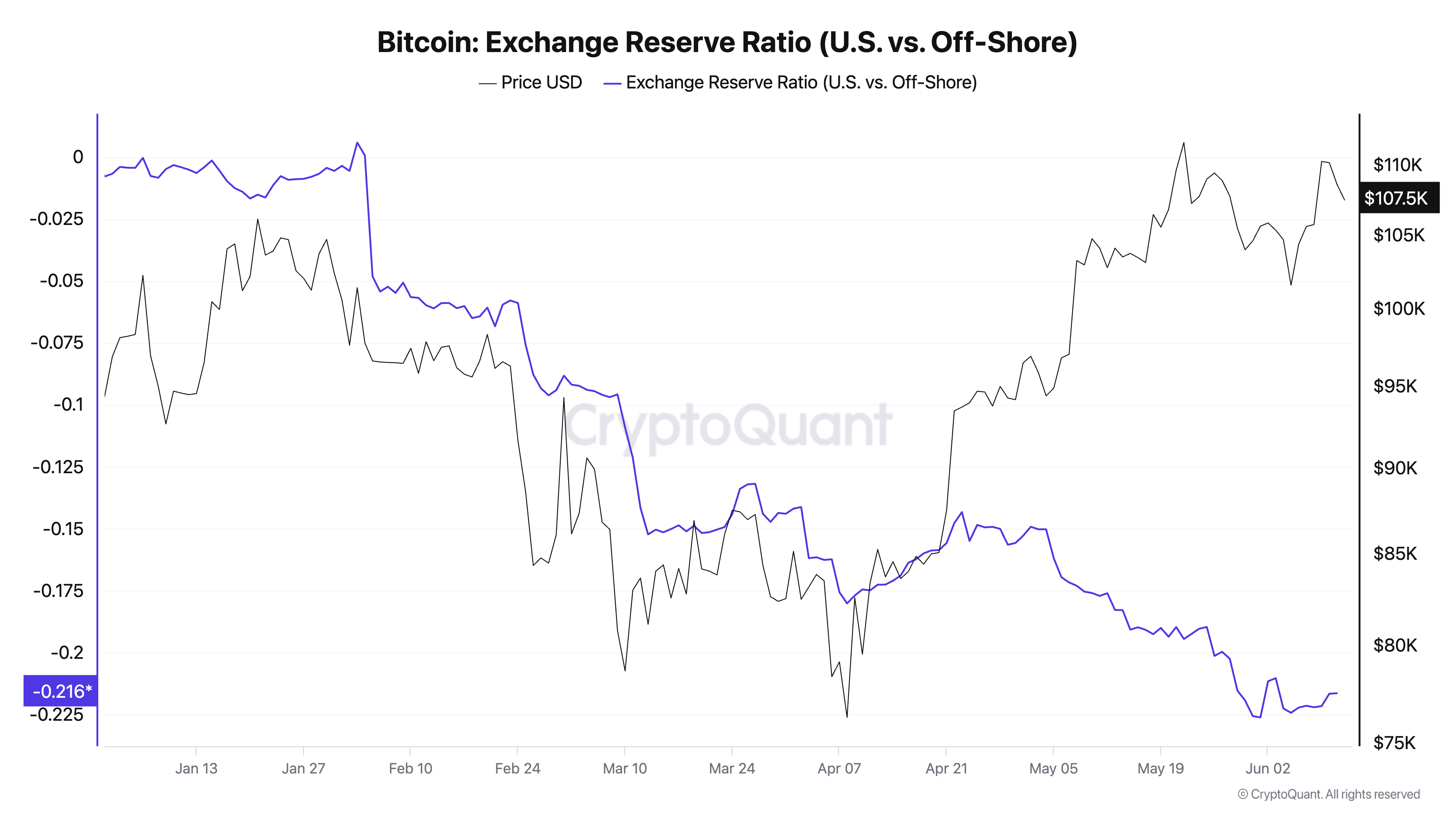

The same pattern appears when comparing reserves on the exchanges of the United States to marine places. For the first time in years, maritime exchanges bear more than its counterparts in the United States, as the backup rate in the United States/Navy fluctuates on January 1 and decreases to -0.22 by mid -June.

The frequency of this decline remained stable throughout the Bitcoin gathering in the first quarter and the subsequent monotheism in the second quarter, with little evidence that the prominent approval of the investment funds circulated last year or the cancellation of SAB 121 contrary to the direction.

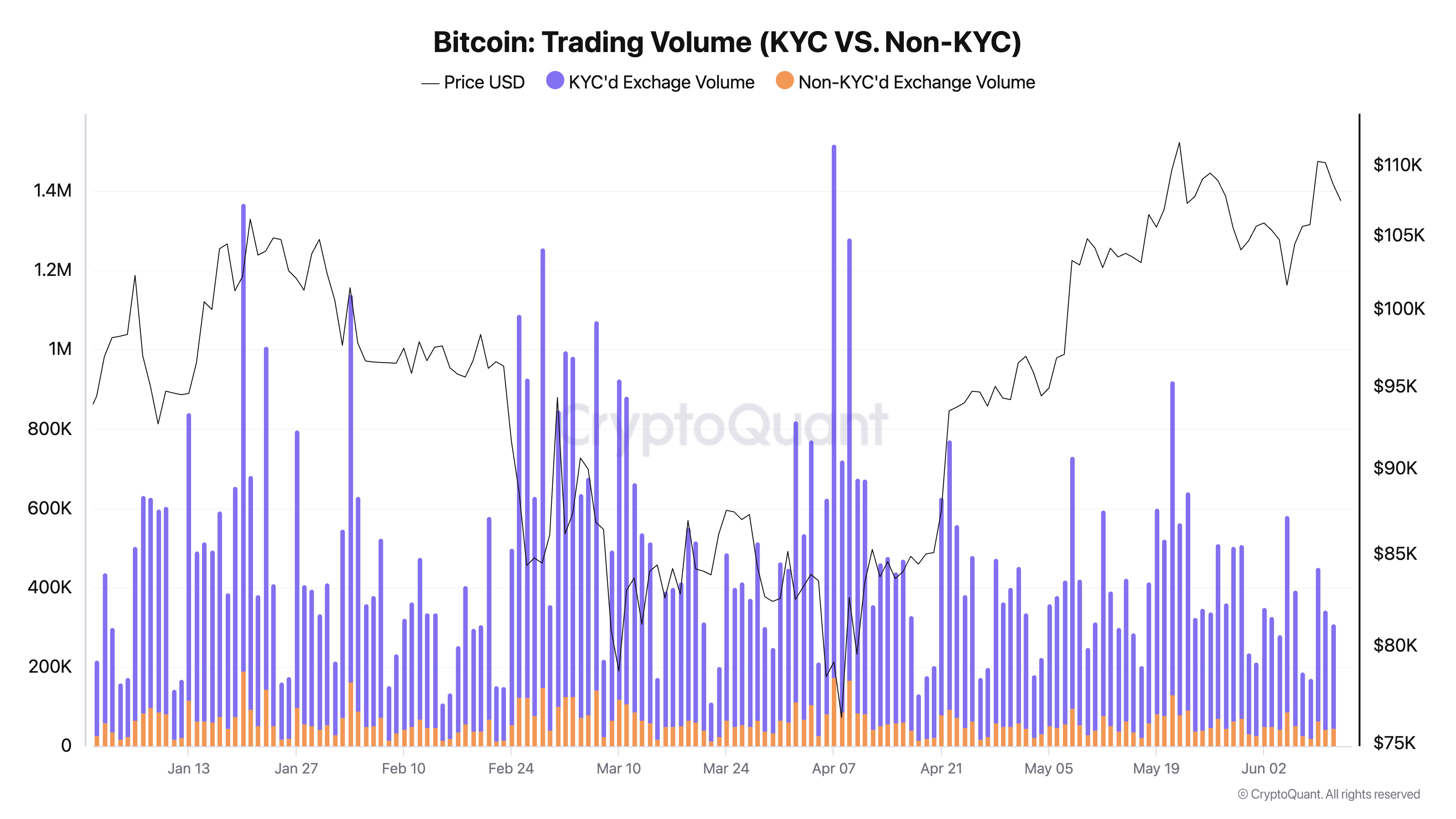

Size patterns enhance this shift. The daily trading volume on KYC compatible platforms decreased by 18.6 % between January and June, as it decreased from an average of $ 424,700 from BTC per day to $ 345,800. The non -kyc exchanges have also seen slowing, as the average volume sizes decreased by 15.3 %, but their share of total topical activity increased from 12.8 % to 14.5 %. This accurate increase indicates a high (or preference) to trade outside the traditional regulatory frameworks.

The difference between price and backup raises major structural questions. The Bitcoin price estimation did not coincide with a renewed flow of reserves for us or KYC places. In fact, the levels of reserves and price data are associated with only weak: KYC/other than KYC shows only +05 only at the price of Bitcoin, while the US/external ratio in +03. This link is a link that these transformations are not just reactions to market gains, but they are part of a deeper reorganization in market behavior.

External stock exchanges, especially those -based states, continue with the requirements of the Laxer identity verification, to attract both high -frequency market makers and retail users who are looking for more unveiling or more lenient trading conditions. Low fees and access to the broader, wide symbol of these platforms play a role, especially with the return of neutral and constitutional strategies against the background of the expanded options market.

Although ETF flows were purely positive from year to date, they were not accompanied by a continuous accumulation of reserves on American exchanges. Instead, reserves have been flat or refused, indicating that a lot of the purchase of the European Union is directed directly through the credit participants who use the current liquidity. It also shows that this purchase failed to create a meaningful request for the immediate acquisition of the stock exchanges.

This indicates the paradox: the infrastructure that has been built to give legitimacy to Bitcoin and its merged into the American financial markets may accelerate the depletion of custody and circulation away from the American platforms. The circulating investment funds provide an easy exposure to the price, but they separate this exposure from the basic currency movement that once helped consolidate this liquidity in the United States.

The elasticity of other Kycc and Offshore activity can create major changes in the market. The increasing share of trading volume outside the traditional compliance bars may complicate the enforcement procedures, scoring measures, and challenge assumptions on the centrality of American platforms in discovering driving prices.

However, the data shows that the adoption of Bitcoin as a financial tool has not been tampered with its decentralized nature. Even amid the increase in institutional interests and ETF flows that have shattered the records, the nursery and liquidity preferences are drifted towards a less resistant path. The United States may remain a major entry point for FIAT CAPITAL, but access to Bitcoin’s trading still extends abroad, beyond the border, increasingly outside the reach of the organizers.

Pamphlet Bitcoin’s liquidity is transmitted to other KYC exchanges, where the United States maintains twice First appear on Cryptoslate.