Bitcoin The price erased recent gains, falling nearly 5% to below $87,000 in early Asian trading hours on December 1.

This came as rising Japanese government bond yields sparked a widespread sense of risk aversion, shattering the fragile, low-volume market structure.

according to Cryptocellite Data, BTC fell from a The consolidation range is near $91,000Which wiped out nearly $150 billion from the total market value of cryptocurrencies.

Carry trade in Japan Repricing continued the decline, but trading volume data showed that the sell-off was exacerbated by a market operating with minimal liquidity.

According to 10x Research, the cryptocurrency market just had one of the lowest weeks in terms of volume since July, leaving order books dangerously thin and unable to absorb institutional selling pressure.

Therefore, Bitcoin’s decline was not just a reaction to the headlines, but a structural failure at a key resistance level.

Vacuum volume

under Bitcoin’s $3.1 trillion market cap surfacedwhich rose 4% on a weekly basis, liquidity appears to have evaporated.

Data from 10x Research indicates that average weekly volumes have fallen to $127 billion. Bitcoin trading volumes specifically fell by 31% to $59.9 billion, while Ethereum trading volumes collapsed by 43%.

This lack of engagement turned what could have been a record technical correction into a liquidity event.

Timothy Messer, head of research at BRN, said: Cryptocellite That this was not a “calculated correction.” Instead, he painted it as a “liquidity event driven by positioning and macro repricing.”

He also noted that momentum “suddenly flipped” after a chaotic November, creating a deep gap down that led to a flood of leveraged buy trades. It was November Worst performing month for Bitcoin This year, it lost approximately 18% of its value.

As a result, shallow market depth meant that what could have been a 2% move during a high-volume week turned into a 5% pullback during an illiquid weekend window.

A tale of two leverages

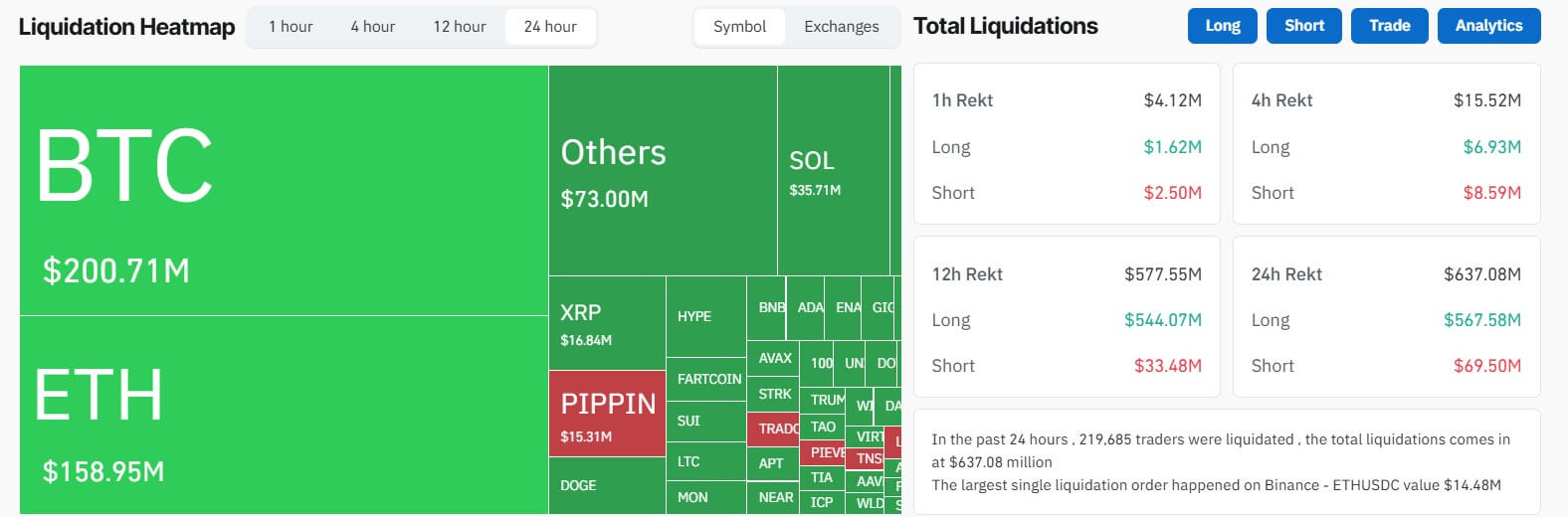

The current price decline has led to a large number of liquidations, with approximately 220,000 cryptocurrency traders losing $636.69 million.

However, the sell-off also revealed a serious difference in how traders position themselves across top crypto assets.

10x Research reported that Bitcoin traders were risk averse, while… Ethereum Traders have been aggressively adding leverage. This has created an unbalanced risk profile in the financial derivatives market.

According to the company, open interest in Bitcoin futures fell by $1.1 billion to $29.7 billion before declining, with funding rates rising modestly to 4.3%, putting it in the 20th percentile over the past 12 months.

This suggests that the Bitcoin market was relatively “great” and that exposure was on the decline.

On the other hand, ETH is now issuing warning signals.

Although network activity is essentially dormant, with gas fees at the fifth percentile of usage, speculative enthusiasm has increased into overdrive.

Funding rates rose to 20.4%, putting cost of leverage in the 83rd percentile from last year, while open interest rose by $900 million.

This disconnect, with Ethereum seeing “frothy” speculative demand despite the collapse of the network instrument, suggests that the market is mispricing risk.

Macro triggers

While market structure provided the fuel, the spark arrived from Tokyo.

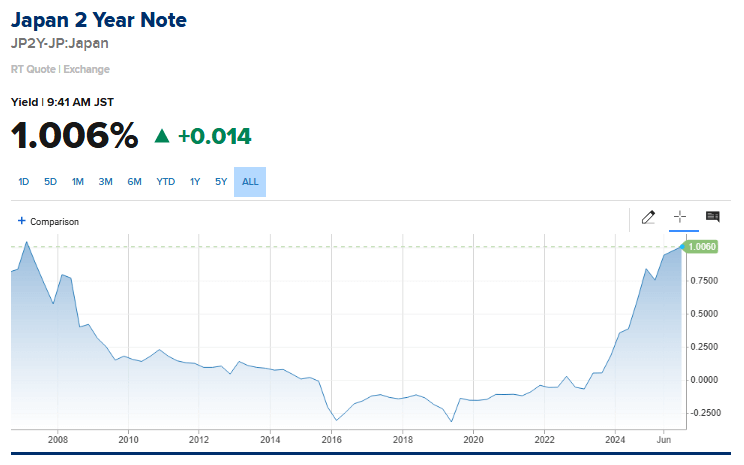

The yield on Japanese government bonds for 10 years rose to 1.84%, a level not seen since April 2008, while the yield on two years exceeded 1% for the first time since the global financial crisis in 2008.

These moves have led to a repricing of expectations for the Bank of Japan’s monetary policy, with markets increasingly pricing in an interest rate hike in mid-December. This threatens the “yen carry trade,” where investors borrow cheap yen to finance risky assets.

Arthur Hayesco-founder of BitMEX, male The Bank of Japan “raised interest rates in December, strengthening the yen and raising the cost of capital for global speculators.

But the overall concern is not limited to Japan.

BRN’s Messer points to gold’s continued rise to $4,250 as evidence that global traders are hedging against persistent inflation or rising financial risks. He pointed out:

“When overall liquidity shrinks, cryptocurrencies, a high-beta asset, often retest the lower bands first.”

With US employment data and ISM publications due later in the week, the market is challenged by “event risks” that could further pressure already low liquidity.

Retail distress and on-chain reality

The fallout has hurt Bitcoin’s technical picture, pushing the price below its “short-term holder cost basis,” a critical level that often distinguishes between bull market declines and deeper corrections.

Cross-chain flows paint a picture of distribution from smart money to retail hands.

According to BRN analysis, accumulation by Long-term holders and large portfolios have slowed down. Instead, retail groups with less than 1 BTC were buying at “distressed levels.”

While this indicates some demand, the absence of whale accumulation suggests that institutional investors are waiting for prices to decline.

Masir said:

“The key takeaway is that supply has shifted into stronger hands, but excess supply remains above key resistance bands.”

However, there is a fair amount of “dry powder” on the margin. Stablecoin balances on exchanges have risen, indicating that traders have capital ready to deploy. But as Bitcoin futures traders disband ETFs are largely offline During the weekend decline, capital has not yet intervened strongly.

Given this, the market is now looking towards the $80,000 level for structural support.

However, failure to reclaim the $90,000 low would suggest the weekend liquidity flow will continue further, likely targeting the $80,000 low, as the yen unwinding carries trade ripples through the system.