No one has a crystal ball, but if Bitcoin continues to behave according to its previous cycles, it is likely that we have already reached the peak.

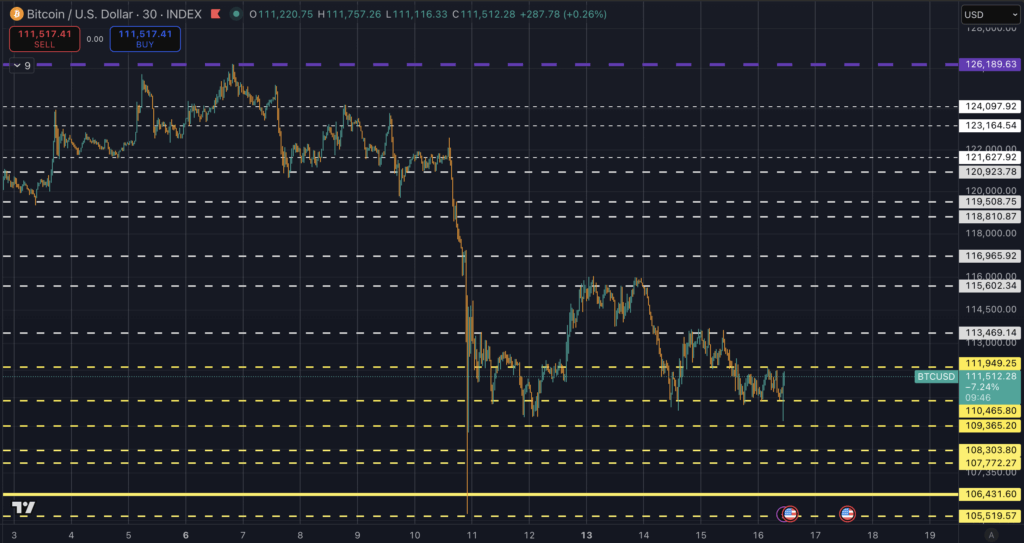

Bitcoin hit an all-time high on October 6, but failed to extend this move as the post-half hour approached the peak zone seen in previous sessions.

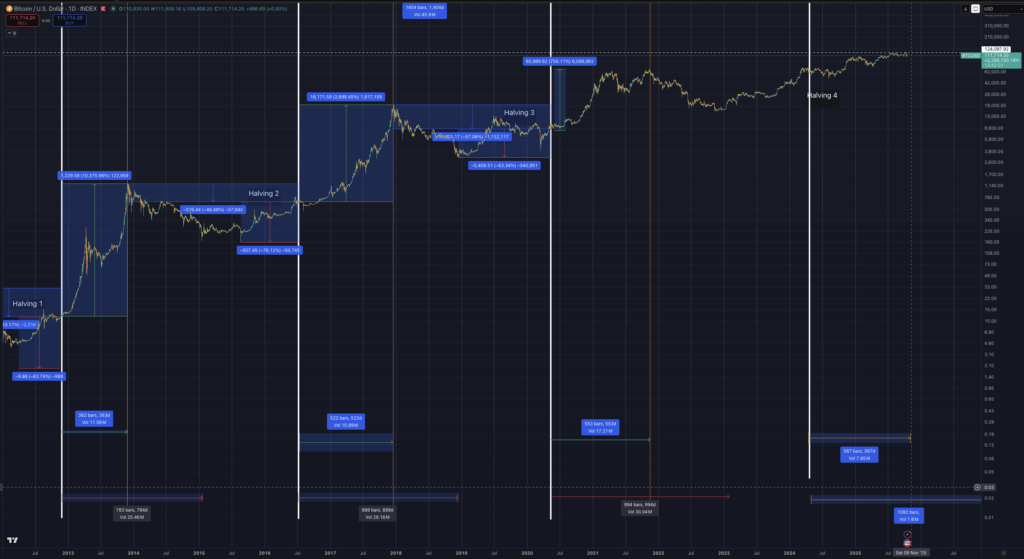

The 2024 halving hit on April 20, with previous peaks reached approximately 526 days after the halving in 2016 and 546 days after the halving in 2020.

In this rhythm, the peak window of the current cycle extends approximately from mid-October to late November.

The October 6 print near $126,200 has not been recovered, with spot trading between $105,000 to $114,000 and key support near $108,000.

The timing situation now intersects with a clear macro shock.

Since the all-time high, the White House has announced a new tariff package on Chinese imports, including rates of up to 100% on some goods. The headline hit cryptocurrencies as futures shaved off nearly $19 billion in liquidations within 24 hours.

Derivatives positions have also shifted, with increased demand for downside protection after liquidation. Financing pressures on the traditional side have also diminished Reuters The bank announced an unusual jump in the use of the Federal Reserve’s permanent repo facility, a signal of tightening short-term dollar funding in the same window.

The flow bar remains the arbiter of the near term. US Bitcoin exchange-traded funds acted as marginal buyers of the session. Persian investors It publishes consolidated daily creations and redemptions that allow a quick read on whether cash is coming in or out of the wrapper.

Weekly fund flow context is provided by Currency stockswhich tracks broader digital asset products. A series of broad net flows over several sessions would keep the door open for a marginal late-session rally.

A choppy move to the negative would strengthen the argument that October 6 marks the top of the cycle.

The scenario framework helps translate those inputs into prices and time.

Bitcoin’s historic bear wave lasted about 12 to 18 months and fell approximately 57% in 2018 and 76% in 2014 from peak to trough, a pattern charted by necessary.

The market structure now includes spot ETFs and deeper derivatives markets, so the lighter 35 to 55 percent range is a reasonable reference for managing downside risk. It is applied to $126,272, producing bottom areas of about $82,000 to $57,000.

This timeline would place the low sometime in late 2026 to early 2027, broadly in line with the halving rhythm noted above.

The probability that there will actually be a peak increases when the timing, macro, and flow tend the same way. A half hour is late in the typical range.

The tariff shock has created uncertainty in the real economy and a clear risk premium in financial derivatives. The use of repurchase facilities jumped to tighten dollar liquidity.

Bitcoin price The pair failed to maintain the early October high and is now trading below the first support level. The burden of proof is on the demand, and the ETF ticker is the cleanest daily measure.

Some argue that traditional Bitcoin The course is over When ETFs were launched, however, new demand did not end the cyclical pattern of the past. Would he really do it now?

So far, every Bitcoin cycle has delivered diminishing returns. If $126,000 were indeed the peak for this cycle, it would result in a gain of 82%.

| From previous top → new top | Previous ATH ($) | New ATH ($) | % profit from previous high |

|---|---|---|---|

| 2011 → 2013 | 31 | 1,177 | 3,696.8% |

| 2013 → 2017 | 1,177 | 19,783 | 1,580.8% |

| 2017 → 2021 | 19,783 | 69,000 | 248.6% |

| 2021 → 2025 (assumed) | 69,000 | 126,000 | 82.6% |

The first decline (Cycle 1 → 2) saw a decline in returns of approximately 57%.

The next decline (Cycle 2 → 3) saw another decline of approximately 84%.

If this rate of dissolution had continued proportionately (about 70% to 80% less each cycle), the expected return would have been about 50% to 70%, not 82%.

So, the potential gain of 82% actually represents a slight decline compared to the exponential decay pattern indicated by previous cycles.

The relative return for this cycle is above trend, which may indicate a mature but still resilient cycle, even if this is the top.

| Cycle transition | Previous gains (%) | Next profit (%) | Fall rate | The percentage retained from the previous cycle |

|---|---|---|---|---|

| 2011-2013 → 2013-2017 | 3,696.8 | 1,580.8 | 0.43 | 43% |

| 2013-2017 → 2017-2021 | 1,580.8 | 248.6 | 0.16 | 16% |

| 2017-2021 → 2021-2025 | 248.6 | 82.6 | 0.33 | 33% |

While historical returns show a clear decay curve, this cycle’s potential gain of 82% slightly breaks the expected downward slope, indicating either the beginning of a slower decay phase or structural changes (e.g., demand for ETFs, institutional capital) moderating the long-term diminishing return trend.

The opposite case requires a specific sequence.

A five- to 10-day series of broad net creations across the ETF pool would show sustained cash demand.

Options skew will need to focus back toward calls for more than just a passing bounce, a shift that third-party dashboards like lightness

The spot price would then need to clear and hold above $126,272 as trading volume increases.

This path could lead to a new marginal high in the $135,000 to $155,000 region before distribution resumes, a pattern echoed in our past. Course comments.

If these conditions do not develop by the end of the traditional window of 518 to 580 days, time itself becomes a headwind.

Miners add another forward signal. Post-halving revenues per unit of retail were compressed, and the share of fees adjusted from spring highs, tightening cash flow for older fleets. This is followed by the dynamics of the economy and fleet turnover Hashrate indicator.

If the price weakens while energy costs remain constant, periodic sell-offs by miners to cover operating costs and service debts may emerge. This supply tends to meet weak demands after shocks. On-chain assessment ranges such as MVRV and MVRV-Z help determine late cycle risk, although absolute limits vary by cycle and should not be used in isolation.

Macro holds his own scoreboard.

The dollar’s path reacts to risk appetite, and Reuters Forex wraps provide a continuous reading of relative strength. Price forecasts are tracked by CME FedWatchThis helps explain whether the tariff shock and any subsequent inflationary pressures change the course of policy.

If easing expectations decline while repo facilities remain high, liquidity for speculative assets could remain constrained.

Readers can follow the framework through the table below.

| scenario | Conditions for viewing | Reasonable path | Price range and timing | What is invalidated? |

|---|---|---|---|---|

| Already higher in | ETFs roll flat into negative, extreme skew persists, and dollar liquidity tightens. | Sideways distribution from 94K to 122K, then collapse on repeated closes below ~108K | Withdrawal from 35% to 55% of ATH, from 82k to 57k, within 12-18 months | Five to ten straight days of broad ETF flows, skewed volatility, and a decisive close above $126,272. |

| Late marginal rise | Multi-session ETF builds, quieter trading headlines, and a weaker dollar. | Fast push via ATH, fails on second attempt, back in range | 135k to 155k in the fourth quarter, then it means a bounce | Return of outflows and sustained demand |

| Extended superstructure | Mixed ETF flows, contained volatility, and continued macro noise | The range is trading between 100K and 125K until late November, which is the highest level based on time | The second attempt was postponed until early 2026, then distribution | Strong, sustainable net innovations or clear scale breakthrough |

Leverage profile calls for patience. Traders added bearish hedges after the tariff shock rather than chasing the upside. This is consistent with a market that focuses more on capital preservation than momentum.

If ETF flows do not resume quickly, traders’ hedging flows from buying can keep the rallies contained. If flows resume, the structure can change quickly, which is why the bar needs daily attention.

None of this diminishes the structural supply of Bitcoin created by the ETF wrapper or the long-term impact of fixed supply. It sets the late cycle setting which now holds total pressure. The halving timer is approaching the end of its historical window.

The October 6 high is considered the price to beat. Until the flows change the equilibrium, the state of the distribution remains the cleanest reading.