For two years, DeFi has worked on the concept that purely local crypto assets could serve as the monetary base of a parallel financial system.

Ethereum deposited through Lido with billions of dollars in DeFi loans, wrapped Bitcoin Backed perpetual swaps and algorithmic stablecoins have recycled the protocol’s emissions into synthetic dollars.

The entire edifice assumed that cryptocurrencies could pave its own collateral hierarchy without touching the $27 trillion US Treasury bond market.

This assumption has been quietly shattered over the past eighteen months. US Treasuries and money market token funds are now worth nearly $9 billion across 60 distinct products and more than 57,000 holder addresses, with an average seven-day return of close to 3.8%. The growth in this period was more than five-fold.

Zoom out to the entire pool of real assets and the value of tokenized RWAs on public chains is worth $19 billion, with government securities and income products dominating, according to rwa.xyz Data.

Treasuries have become the backbone of this stack, functionally replicating their role in the $5 trillion US repo market, the vehicle through which everything else is settled.

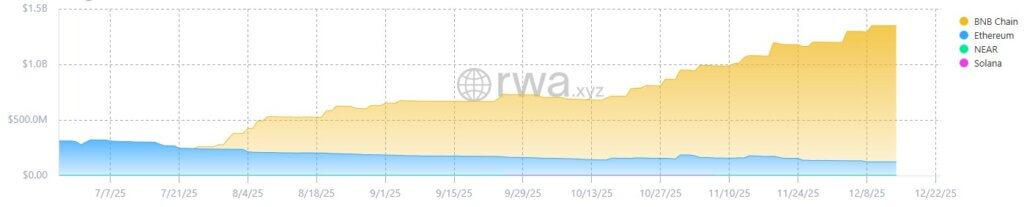

This is not a boutique experience. Black Rock BUIDL box has arrived Its size is approximately $3 billionwas accepted as a guarantee on Binanceand was extended to the BNB chain.

Franklin Templeton The BENJI token represents over $800 million in US-registered government money market funds, with shareholder records maintained on seven different networks.

Circle USYC quietly surpassed $1.3 billion in July, boosted by a partnership with Binance that enabled institutional investors to use the token as collateral for derivatives trading.

JP Morgan Launched a $100 million tokenized money market fund Ethereum Which allows qualified investors to subscribe and redeem in USDC. The plumbing connecting Wall Street custody to Ethereum rails is in production, not a proof of concept.

Wall Street custody meets Ethereum settlement

The issuer landscape reveals two competing theories about how cryptocurrency collateral will evolve.

BlackRock’s BUIDL acts as a tokenized institutional liquidity fund that it manages Securitizationwith Bank of New York Mellon Handling custody and fund management. Stocks represented by the BUIDL token invest in cash, US Treasuries, and repurchase agreements.

Redemptions are made in USDC, with a minimum of $250,000 and no redemption fees, putting BUIDL directly on the institutional track. Its acceptance as collateral on centralized exchanges and its extension to multiple chains makes it a high-quality dollar-denominated collateral for cryptocurrency derivatives and fundamental trades.

Franklin Templeton has taken a different tack with its OnChain US Government Money Fund, which tokenizes the shareholder registry itself: one share equals one BENJI token, keeping transfer and recordkeeping on-chain instead of the old transfer agent database.

The fund remains a registered U.S. government money market fund, and the innovation is where the ledger is.

This approach bets that public blockchains can serve as a primary ledger for regulated securities, not just a secondary token layer on top of traditional systems.

Janus Henderson Anemoy Treasury Fund Ondo OUSG Financial Group is located on opposite sides of the third axis. Anemoy deploys tokens across Ethereum, Base, Arbitrum, and Celo, focusing on cross-chain flexibility, and has received an S&P rating focused on its token architecture.

In contrast, Ondo acts as a native decentralized finance (DeFi) issuer in partnership with back-end institutions. Its OUSG product offers 24/7 minting and redemptions in PayPal’s USDC or PYUSD currency, targeting qualified investors who want treasury exposure without leaving the trails of native cryptocurrencies.

The broader Ondo platform reached $1.4 billion in total value by mid-2025, nearly half of which was tied to tokenized treasury products, and has since expanded into multiple chains.

Small exporters fill the tail of composability. Matrixdock’s STBT resets interest rates daily and maintains a one-to-one peg to the dollar, backed by Treasury bills maturing in six months and reverse repurchase agreements.

OpenEden The TBILL token has a Moody’s rating of “A” and can be used as collateral in DeFi protocols.

on Solanaapproximately $530 million of the $792 million of tokenized real assets are US Treasury securities, with Ondo’s US dollars It holds approximately $175 million and behaves like an interest-bearing stablecoin within Solana DeFi applications.

Redemption mechanics restrict composability

Mechanically, most coded cabinet products follow the same spine. A structured fund or special purpose vehicle holds short-term U.S. government securities and repurchases with a traditional custodian, such as the Bank of New York Mellon.

The transfer agent or tokenization platform mints ERC-20 or similar tokens representing Fund shares, registered on Ethereum or other layer-one blockchains.

Franklin’s BENJI maintains the on-chain shareholder registry. Meanwhile, OpenEden’s BUIDL and TBILL keep securities custody and money management firmly within traditional fiduciary structures, issuing tokens representing economic claims.

Ondo’s OUSG offers instant 24/7 mints and redemptions in USDC or PYUSD, with the number of tokens multiplied by the NAV to determine what the investor receives.

These are not CUSIP codes that someone can burn to get a Treasury bill at the Fed. They are tokenized fund shares with specific redemption windows, minimum sizes, and KYC requirements, even if the tokens themselves reside on public blockchains.

This distinction limits composability. Many of these tokens are on permissioned smart contracts, and only KYC’d wallets can hold or transfer them. Some have minimum redemption sizes in the six-figure range, and full composability is often limited to “KYC-DeFi” venues rather than unauthorized public pools.

However, within these constraints, composability advances in two layers. At the institutional level, tokenized treasury funds act as margin collateral.

Treasury funds and money market tokens are increasingly being used as collateral for over-the-counter derivatives, allowing traders to move collateral 24/7 rather than being tied to bank business hours, the Financial Times reported.

USYC’s growth is another sign, as it has grown nearly six-fold since Circle and Binance partnered.

At the DeFi layer, integration is more fragmented but real. OpenEden’s TBILL tokens can be deployed as collateral in DeFi lending protocols like River, with secondary liquidity on decentralized exchanges and RWA markets.

Matrixdock’s STBT integrates with RWA yield platforms, offering approximately 5% APY on short-term Treasuries, with instant mintage and redemption in coordination with stablecoins like Ripple’s RLUSD.

MakerDAO held approximately $900 million of RWA collateral, mostly from US Treasuries, by mid-2025, with plans to increase this stake under the new Sky Protocol brand.

Frax’s sFRAX vault purchases US Treasuries directly through a partner bank and passes them through a yield that tracks the overnight repo rate. Tens of millions of sFRAX were deposited, generating a return of nearly 5%.

Protocols like Pendle treat yielding collateral, including RWA-backed stablecoins and sDAI, as inputs to the on-chain interest rate curve by splitting the principal and yield into separate tokens.

With the proliferation of Treasury bill tokens and treasury-backed stablecoins, Pendle and similar markets have become the price discovery layer for short-term rates in DeFi.

At Solana, more than 50% of token assets traded are US Treasuries, with Ondo’s USDY and OUSG among the largest positions, according to Devilama data.

Ethereum serves as the regulatory backbone, with BUIDL, BENJI, and Anemoy, while Solana acts as a high-throughput rail where treasury-backed tokens behave almost like interest-bearing stablecoins in DeFi applications.

Regulatory friction and systemic risk

The regulatory structure revolves around three questions: who can hold these tokens, where they are registered, and how they intersect with stablecoin rules.

Most large issuers operate as money market funds or professional funds under current securities law. BENJI/FOBXX is a government money market fund registered in the United States.

OpenEden’s TBILL Fund is a professional fund regulated by the BVI and supervised by the BVI Financial Services Commission. Janus Henderson’s Anemoy received an S&P rating that focuses on token setup and controls.

Regulatory frameworks such as crypto asset markets in the European Union and, in the United States, suggest proposed stablecoin legislation clearly refers to treasuries and tokenized money market funds, providing clarity to issuers on wrapping government debt in tokens.

However, most of this composability remains permissible. KYC-DeFi venues, not unauthorized public gatherings, host the majority of integrations.

When it comes to systemic risk, convergence with stablecoins is most important. Going back to mid-2024, Circle held approximately $28.1 billion in short-term U.S. Treasuries and overnight reverse repos of USDC reserves, out of a total of $28.6 billion in reserves.

Even before Treasuries became popular on-chain as freely transferable tokens, they were already an invisible security behind systemically important stablecoins.

Tokenization makes collateral itself portable, pledgeable, and in some cases, composable as DeFi money.

In short, stablecoins actually turn Treasuries into money as reserve assets. Tokenized treasury funds now bring those collaterals on-chain, where they can be remortgaged, sidelined, and structured into structured price and product curves.

Return cycle or structural transformation

There are two forces that explain the growth path. On the cyclical side, the 2023-2025 price environment provided a clear tailwind.

Front-end yields in the US range from 4% to 5%, making treasury tokens a clear upgrade over zero-yielding stablecoins, especially for market-making companies and DAOs that need to store idle cash on-chain.

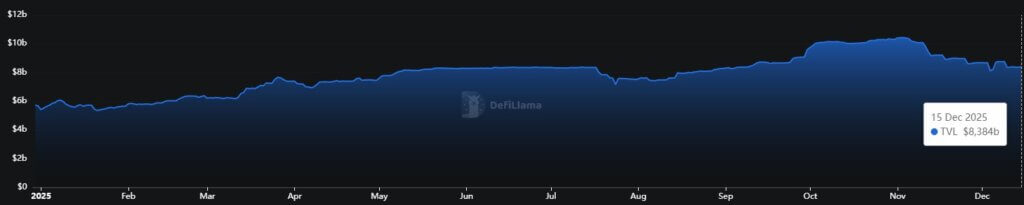

Issuances rose from about $1.3 billion in early 2024 to $9 billion as of December 15, closely tracking the rise in front-end interest rates.

On the structural side, several data points suggest that this extends beyond price cycle trading. Total tokenized RWAs on public chains have exceeded $18.5 billion, with government debt as an anchor.

Tokenized treasury funds have become an accepted collateral for cryptocurrency derivatives and central exchange margin, and institutions like JPMorgan are launching tokenized money market funds on Ethereum explicitly to take advantage of 24/7 settlement and stablecoins.

DeFi’s monetary base has quietly shifted from pure cryptocurrencies to a mix of stablecoins and RWA-backed instruments. Meeker, Frakes and others increasingly rely on Treasuries and repurchase agreements as collateral.

Pendle and similar protocols build on-chain rate curves that reference those instruments.

Solana’s RWA landscape is dominated by treasury-backed tokens that behave like yield-bearing stablecoins within DeFi applications.

Tokenized Treasuries are evolving into the repo market for cryptocurrencies: an underlying layer of dollar-backed, state-backed collateral against which everything else, such as perpetual swaps, underlying trades, stablecoin issuance, and prediction market margining, will increasingly dwindle.

Turning today’s $9 billion into $80 billion depends on regulation and prices, but the plumbing is in production on Ethereum and Solana. The question is no longer whether TradFi collateral migrates on-chain, but how quickly DeFi protocols will reconnect around it.